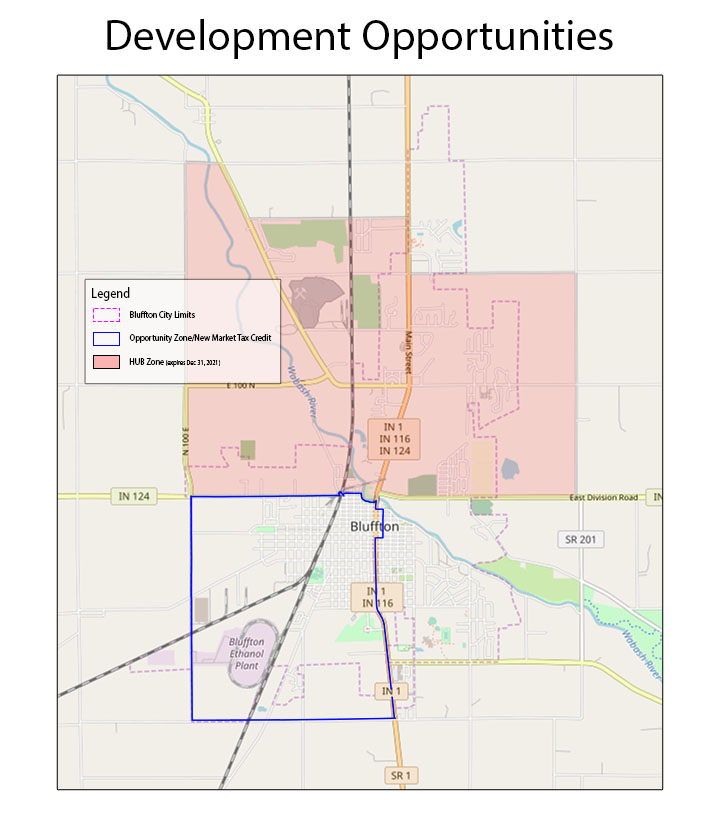

Investment Zones

Areas near and within the city limits of Bluffton, Indiana provide numerous opportunities for investment assistance. Investment assistance is available through a HUB Zone designation and New Market Tax Credit Program. Each of these areas offer unique opportunities to develop, grow, and investment in a business in Wells County, Indiana.

HUBZone Characteristics

The government limits competition for certain contracts to businesses in historically underutilized business zones. It also gives preferential consideration to those businesses in full and open competition. Joining the HUBZone program makes your business eligible to compete for the program’s set-aside contracts. HUBZone-certified businesses also get a 10 percent price evaluation preference in full and open contract competitions.

To qualify for the HUBZone program, your business must:

- Be a small business

- Be at least 51 percent owned and controlled by U.S. citizens, a Community Development Corporation, an agricultural cooperative, a Native Hawaiian organization, or an Indian tribe

- Have its principal office located in a HUBZone

- Have at least 35 percent of its employees live in a HUBZone

You can find the full qualification criteria in Title 13 Part 126 Subpart B of the Code of Federal Regulations (CFR). You can also get a preliminary assessment of whether you qualify at the SBA’s Certify website.